")

By D. Thomakos

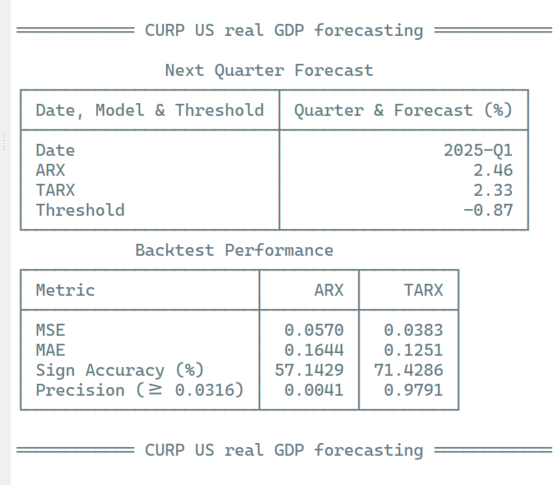

So Stephanos Kechagias, a good friend and seasoned professional in time series analysis, sends me this dire nowcasting prediction for US real GDP growth from the Atlanta Fed, for -2.8% for March 3rd, 2025. Having worked a bit on previous posts on forecasting US real GDP growth, for example see here for the CURP index, I thought that some fun work was in order. I ain't going to give you a nowcasting system but something simpler, which can be considerably customizable and expandable for your own needs.

I pointed DeepSeek to my CURP index post and I asked it to create a forecasting system based on the blog post, with backtesting and real-time forecasting capabilities. After a round of iterations (yes, human intervention is necessary still) and cross-checking on the accuracy of the code, we can all now have a very convenient tool for playing around in generating real-time GDP forecasts. Yes, the code is constrained to the leading indicator variables of the CURP index but has lots of flexibility: you can select weights for constructing the index, the starting date for the estimation/backtesting, the backtesting periods and plotting. I am using two standard models, an ARX model and a threshold TARX model, with automatic threshold selection. The models are only illustrative, and you can add others or modify them easily.

For the backtesting I am using the MSE, MAE and the coefficient of predictive precision that I devised also in a previous post - play around with the parametrizations to see how different forecasts have different properties when evaluated. This is a tool for further exploration, be that in Python coding, research or teaching. Comments and suggestions are always welcomed, and I hope that you will enjoy it. A sample output appears below as is the link for the file in my github repository.